All Categories

Featured

Table of Contents

The drawbacks of boundless financial are often neglected or otherwise discussed in any way (much of the info readily available regarding this idea is from insurance policy agents, which might be a little prejudiced). Only the cash value is expanding at the returns price. You likewise have to pay for the expense of insurance coverage, charges, and costs.

Every irreversible life insurance plan is various, yet it's clear somebody's overall return on every dollar spent on an insurance policy product might not be anywhere close to the reward rate for the plan.

Infinite Banking Example

To offer a really fundamental and theoretical example, let's presume someone is able to gain 3%, generally, for every single dollar they invest in an "infinite financial" insurance coverage product (after all costs and fees). This is double the estimated return of whole life insurance coverage from Consumer Reports of 1.5%. If we think those bucks would be subject to 50% in tax obligations amount to otherwise in the insurance policy product, the tax-adjusted price of return can be 4.5%.

We think greater than typical returns on the whole life product and a very high tax obligation price on bucks not take into the policy (that makes the insurance policy item look far better). The fact for numerous people may be even worse. This fades in comparison to the lasting return of the S&P 500 of over 10%.

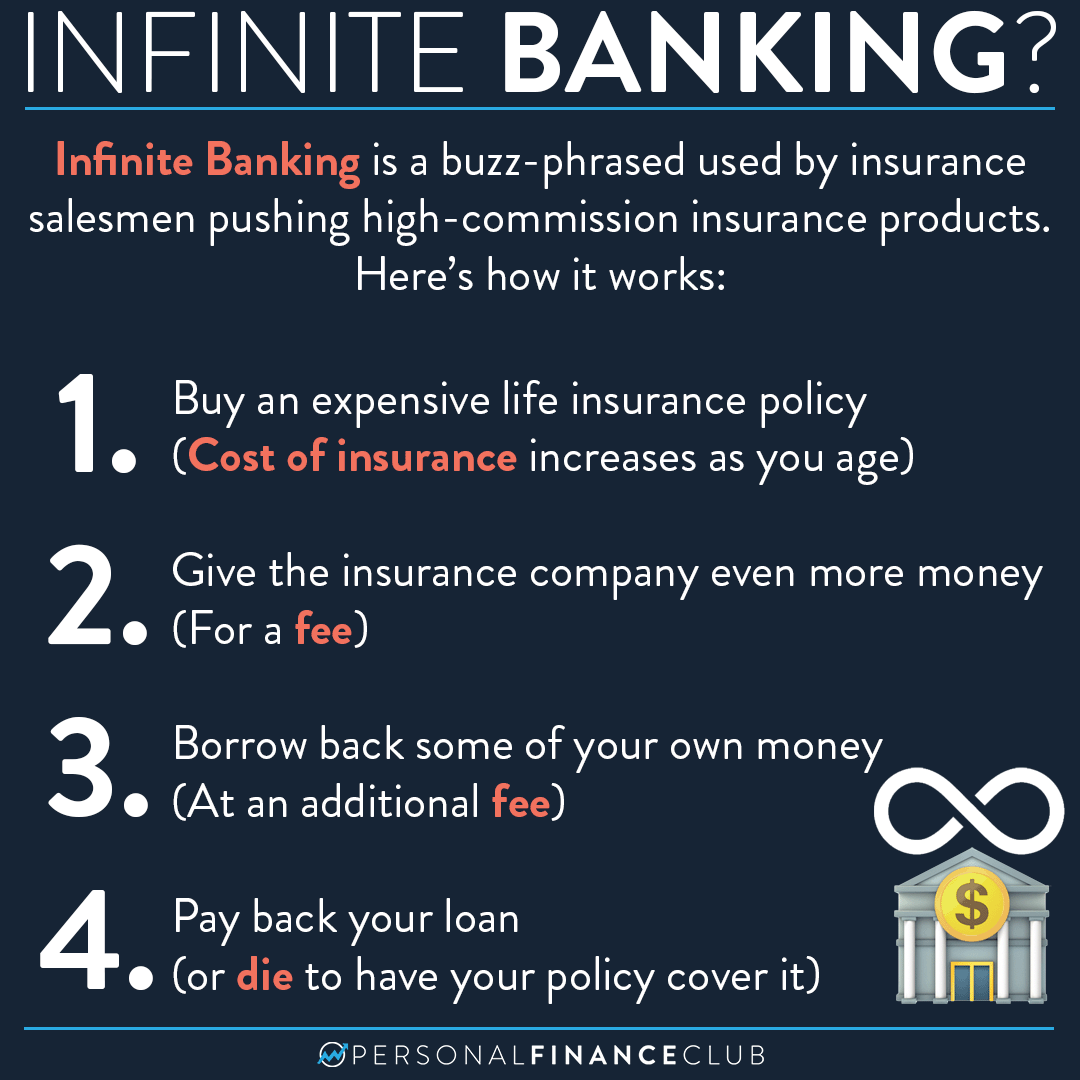

Limitless banking is an excellent item for agents that market insurance policy, however may not be optimal when contrasted to the more affordable alternatives (without any sales people gaining fat compensations). Below's a breakdown of a few of the various other supposed benefits of boundless financial and why they might not be all they're broken up to be.

Infinite Banking Concept Pdf

At the end of the day you are getting an insurance item. We enjoy the protection that insurance policy uses, which can be obtained a lot less expensively from an affordable term life insurance coverage policy. Overdue finances from the plan may also decrease your fatality benefit, decreasing another level of defense in the plan.

The concept only works when you not only pay the considerable costs, yet make use of added money to purchase paid-up enhancements. The chance cost of all of those dollars is significant incredibly so when you might rather be spending in a Roth Individual Retirement Account, HSA, or 401(k). Also when compared to a taxed financial investment account and even a financial savings account, infinite banking might not supply comparable returns (contrasted to spending) and equivalent liquidity, gain access to, and low/no fee framework (compared to a high-yield interest-bearing accounts).

With the increase of TikTok as an information-sharing platform, monetary guidance and methods have located an unique way of dispersing. One such method that has been making the rounds is the unlimited banking idea, or IBC for short, gathering recommendations from stars like rapper Waka Flocka Flame. Nonetheless, while the technique is presently prominent, its origins trace back to the 1980s when economist Nelson Nash presented it to the world.

Within these plans, the cash worth grows based on a price established by the insurer. Once a considerable cash worth collects, insurance policy holders can acquire a cash money worth financing. These car loans vary from traditional ones, with life insurance policy working as security, suggesting one can shed their protection if borrowing exceedingly without ample cash value to support the insurance coverage prices.

Infinite Banking Concept Reviews

And while the allure of these policies is evident, there are innate constraints and risks, necessitating persistent cash money value monitoring. The technique's legitimacy isn't black and white. For high-net-worth individuals or entrepreneur, particularly those making use of techniques like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and substance growth could be appealing.

The allure of infinite banking does not negate its challenges: Cost: The fundamental demand, a permanent life insurance policy plan, is pricier than its term counterparts. Eligibility: Not everyone gets whole life insurance policy because of rigorous underwriting procedures that can leave out those with details wellness or lifestyle problems. Intricacy and danger: The elaborate nature of IBC, paired with its threats, may discourage several, especially when less complex and less dangerous choices are readily available.

Alloting around 10% of your regular monthly income to the policy is just not practical for many people. Utilizing life insurance as an investment and liquidity resource needs discipline and surveillance of plan cash worth. Consult a financial expert to establish if limitless financial aligns with your concerns. Component of what you review below is simply a reiteration of what has already been stated above.

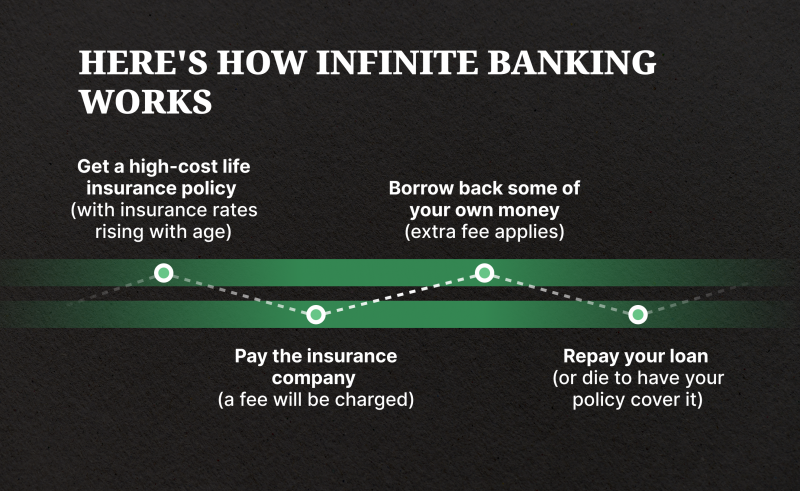

Before you get yourself into a circumstance you're not prepared for, understand the adhering to first: Although the concept is generally sold as such, you're not really taking a financing from on your own. If that were the instance, you would not need to settle it. Rather, you're borrowing from the insurance provider and need to repay it with rate of interest

Is Infinite Banking A Scam

Some social media articles suggest utilizing money value from whole life insurance policy to pay down bank card debt. The concept is that when you pay off the loan with rate of interest, the amount will certainly be sent back to your investments. That's not how it functions. When you repay the funding, a part of that passion goes to the insurer.

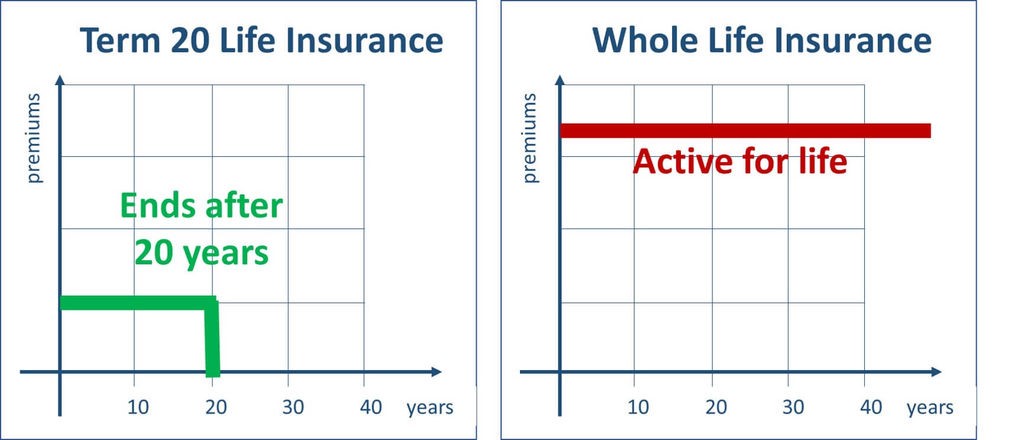

For the initial several years, you'll be paying off the compensation. This makes it exceptionally tough for your policy to accumulate value during this time around. Whole life insurance coverage costs 5 to 15 times extra than term insurance policy. Lots of people simply can not manage it. Unless you can afford to pay a few to numerous hundred bucks for the next years or even more, IBC will not function for you.

If you need life insurance, here are some important suggestions to think about: Take into consideration term life insurance coverage. Make certain to go shopping about for the finest rate.

Infinite financial is not a product and services provided by a details institution. Boundless financial is a technique in which you get a life insurance coverage plan that collects interest-earning money value and get lendings versus it, "borrowing from on your own" as a resource of capital. Ultimately pay back the funding and start the cycle all over once more.

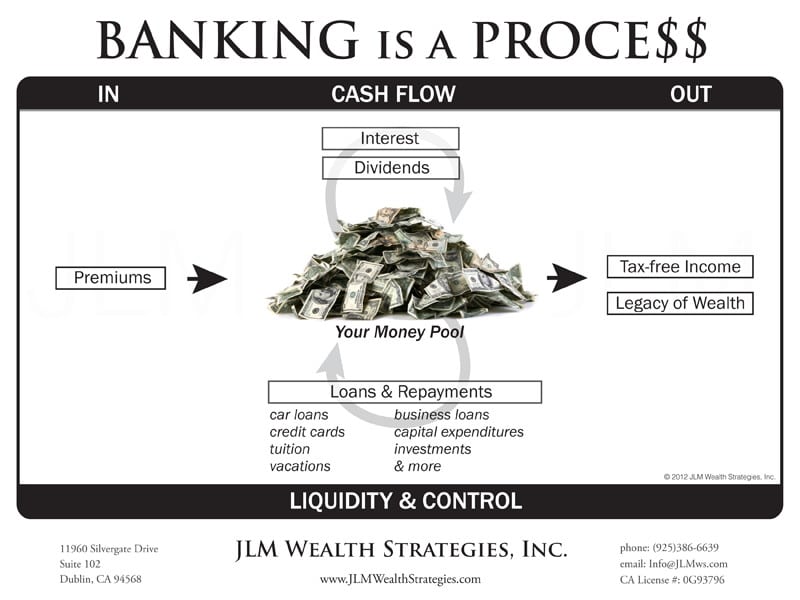

Pay policy premiums, a portion of which builds money value. Cash money worth makes compounding interest. Take a finance out against the plan's cash money value, tax-free. Pay off fundings with rate of interest. Cash money worth builds up again, and the cycle repeats. If you use this idea as intended, you're taking money out of your life insurance policy plan to acquire everything you would certainly need for the rest of your life.

{kind=link}

Latest Posts

Can You Be Your Own Bank

Becoming Your Own Banker And Farming Without The Bank

Bank On Yourself Ripoff